Oak View Bankshares, Inc. Announces 2024 Earnings and Annual Dividend

Rescuers search for missing in China storms after 100,000 evacuated

Rescuers search for missing in China storms after 100,000 evacuated

Ex-Australia cricketer MacGill loses appeal against cocaine conviction

Ex-Australia cricketer MacGill loses appeal against cocaine conviction

Oil prices extend rally as US strikes on Iran revive geopolitical fears

Oil prices extend rally as US strikes on Iran revive geopolitical fears

Iraq's holy cities to host funeral processions for Khamenei

Iraq's holy cities to host funeral processions for Khamenei

In Venezuela's quake ruins, a baby is born

In Venezuela's quake ruins, a baby is born

What to know about the total solar eclipse due in August

What to know about the total solar eclipse due in August

Trump, NATO allies to begin key talks at Turkey summit

Trump, NATO allies to begin key talks at Turkey summit

Former Real Madrid coach Arbeloa named Fulham manager

Former Real Madrid coach Arbeloa named Fulham manager

Messi inspires Argentina great escape over Egypt, Swiss advance

Messi inspires Argentina great escape over Egypt, Swiss advance

US strikes Iran after Hormuz attacks, Tehran threatens response

US strikes Iran after Hormuz attacks, Tehran threatens response

Djokovic wins five-hour epic to earn Sinner showdown at Wimbledon

Djokovic wins five-hour epic to earn Sinner showdown at Wimbledon

US strikes Iran after Hormuz tanker attacks: military

US strikes Iran after Hormuz tanker attacks: military

Messi 'didn't want to go home' as Argentina comeback stuns Egypt

Messi 'didn't want to go home' as Argentina comeback stuns Egypt

Netflix strikes deals in short-form video push

Netflix strikes deals in short-form video push

The height factor: how a small building survived Venezuela's quakes

The height factor: how a small building survived Venezuela's quakes

Egypt 'cheated' in controversial World Cup exit to Messi's Argentina, says Hassan

Egypt 'cheated' in controversial World Cup exit to Messi's Argentina, says Hassan

Global AI industry falls short on safety, think tank warns

Global AI industry falls short on safety, think tank warns

'History made': Egyptian pride despite World Cup heartbreak

'History made': Egyptian pride despite World Cup heartbreak

How rescuers carried out 180-hour 'miracle' amid Venezuela's ruins

How rescuers carried out 180-hour 'miracle' amid Venezuela's ruins

Victorious Belgian footballers troll Trump with YMCA dance

Victorious Belgian footballers troll Trump with YMCA dance

Scotland boss Townsend expects Russell will face Springboks

Scotland boss Townsend expects Russell will face Springboks

Messi inspires Argentina great escape over Egypt

Messi inspires Argentina great escape over Egypt

Zverev, Cobolli targeting rematch at Wimbledon

Zverev, Cobolli targeting rematch at Wimbledon

Colombia president-elect accuses outgoing leader of 'coup' plotting

Colombia president-elect accuses outgoing leader of 'coup' plotting

IOC eases restrictions on Russians before 2028 LA Games as anthem, flag ban remains

IOC eases restrictions on Russians before 2028 LA Games as anthem, flag ban remains

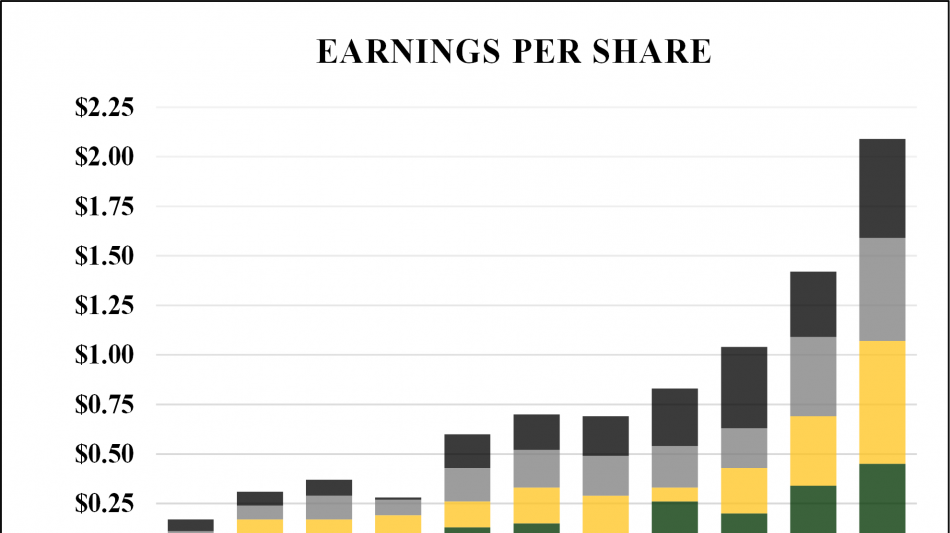

WARRENTON, VA / ACCESS Newswire / January 21, 2025 / Oak View Bankshares, Inc. (the "Company") (OTC PINK:OAKV), parent company of Oak View National Bank (the "Bank"), reported net income of $6.10 million for the year ended December 31, 2024, compared to net income of $4.21 million for the year ended December 31, 2023, an increase of 44.72%.

Basic and diluted earnings per share for the year ended December 31, 2024, were $2.07 compared to $1.43 for the year ended December 31, 2023.

On January 16, 2025, the Board of Directors of the Company declared an annual dividend of $0.27 per share to shareholders of record as of the close of business on January 30, 2025, payable on February 6, 2025.

"Despite industry headwinds and persistent market volatility, our exceptional team delivered 45% growth in earnings per share in 2024. Your Company's strong financial performance reflects our unwavering commitment to striking the optimal balance between safety and soundness, profitability, and growth. We could not be prouder of these results nor more excited about the opportunities that lie ahead," said Michael Ewing, CEO and Chairman of the Board. Mr. Ewing continued, "Oak View National Bank exists to serve our communities and deliver durable and compelling returns to shareholders. We are heartened that our community bank value proposition continues to resonate, which is evidenced by deepening relationships with current clients, steady growth in new relationships, as well as selective additions of talented and trustworthy banking professionals."

Selected Highlights:

Return on average assets was 0.94% and return on average equity was 17.45% for the year ended December 31, 2024, compared to 0.75% and 14.38%, respectively, for the year ended December 31, 2023.

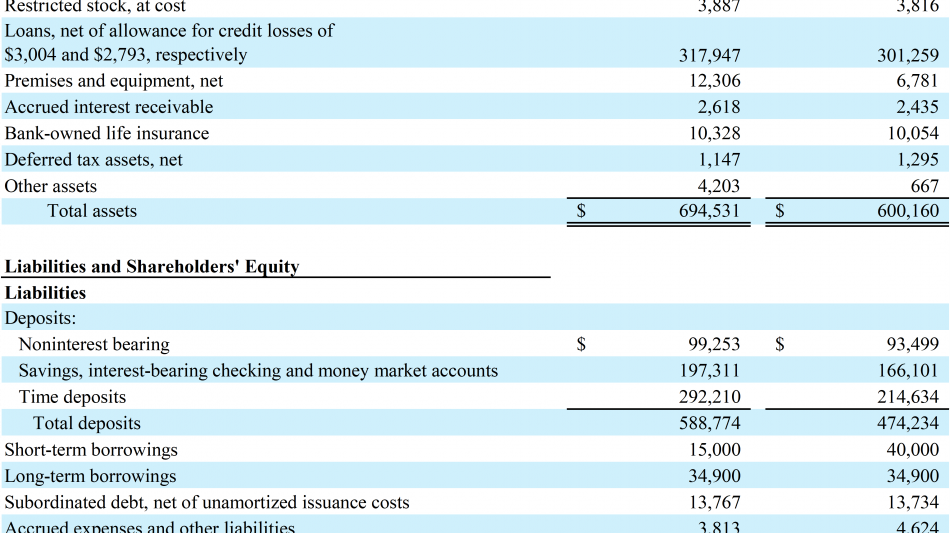

Total assets were $694.53 million on December 31, 2024, compared to $600.16 million on December 31, 2023, an increase of $94.28 million.

Total loans were $320.95 million on December 31, 2024, compared to $304.05 million on December 31, 2023, an increase of $16.90 million. Much of this increase was within the commercial owner-occupied real estate portfolio.

The total amortized cost of debt securities was $297.82 million on December 31, 2024, compared to $248.11 million on December 31, 2023, an increase of $49.71 million.

Total deposits were $588.77 million on December 31, 2024, compared to $474.23 million on December 31, 2023, an increase of $114.54 million. Brokered deposits, all with call options, represent the majority of this growth, while interest bearing demand, money market and time deposits also contributed to the increases within the deposit portfolio.

Regulatory capital remains strong with the Bank's ratios exceeding the "well capitalized" thresholds in all categories, with total capital ratio at 16.56%, common equity tier 1 capital ratio at 15.63%, tier 1 capital ratio at 15.63% and leverage ratio at 7.87%.

Asset quality continues to be outstanding. Net charged-off loans were 0.004% of total loans, there were no nonaccrual loans, accruing loans past due 30-89 days were 0.015% of total loans, and one accruing loan past due 90 days or more was 0.005% of total loans.

Liquidity remains strong with cash, unencumbered securities available for sale, and available secured and unsecured borrowing capacity totaling $505.31 million as of December 31, 2024, compared to $453.94 million as of December 31, 2023.

Net Interest Income

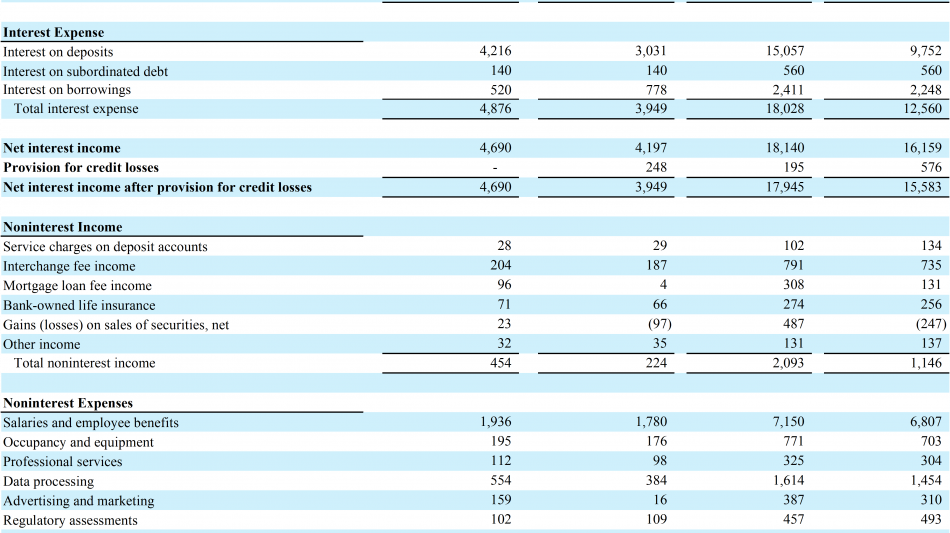

The net interest margin was 2.90% for the year ended December 31, 2024, compared to 2.96% for the year ended December 31, 2023. Net interest income was $18.14 million for the year ended December 31, 2024, compared to $16.16 million for the year ended December 31, 2023. Average earning assets and the related yield increased to $626.64 million and 5.78%, respectively, for the year ended December 31, 2024, compared to $546.23 million and 5.26%, respectively, for the year ended December 31, 2023. Average interest-bearing liabilities, and the related cost of funds, which includes average noninterest bearing deposits, increased to $509.38 million and 2.97%, respectively, for the year ended December 31, 2024, compared to $430.90 million and 2.38%, respectively, for the year ended December 31, 2023.

Noninterest Income

Noninterest income was $2.09 million and $1.15 million for the years ended December 31, 2024, and 2023, respectively, an increase of 82.64%. Net gains from the sales of available for sale securities of $487 thousand contributed to the increase in noninterest income for the year ended December 31, 2024, compared to net losses of $(247) thousand for the year ended December 31, 2023. Proceeds from the sales of securities in 2024 were redeployed into assets with more attractive risk and return characteristics.

Noninterest Expense

Noninterest expenses were $12.41 million and $11.48 million for the year ended December 31, 2024, and 2023, respectively, an increase of 8.08%. Management has consistently exercised robust expense control oversight, even with the Company's growth.

Liquidity

Liquidity remains exceptionally strong with $505.31 million of liquid assets available which included cash, unencumbered securities available for sale, and secured and unsecured borrowing capacity as of December 31, 2024, compared to $453.94 million as of December 31, 2023.

The Company's deposits proved to be stable with core deposits, which are defined as total deposits excluding brokered deposits, of $505.70 million as of December 31, 2024, compared to $443.55 million as of December 31, 2023. Uninsured deposits, those deposits that exceed FDIC insurance limits, were $108.29 million as of December 31, 2024, or 21.41% of total deposits, which management believes is within industry averages.

Asset Quality

The allowance for credit losses related to the loan portfolio was $3.00 million as of December 31, 2024, compared to $2.79 million as of December 31, 2023, or 0.94% and 0.92% of total loans outstanding, net of unearned income, respectively. The increase in the allowance for credit losses related to the loan portfolio was primarily due to loan growth during the year.

Net charged-off loans were 0.004% of total loans, there were no nonaccrual loans, accruing loans past due 30-89 days were 0.015% of total loans, and one accruing loan past due 90 days or more was 0.005% of total loans.

Shareholders' Equity and Regulatory Capital

Shareholders' equity was $38.28 million as of December 31, 2024, compared to $32.67 million as of December 31, 2023. Accumulated other comprehensive loss was $2.51 million as of December 31, 2024, compared to $2.99 million as of December 31, 2023. The unrealized losses reflected therein are primarily related to mark-to-market adjustments on U.S. Treasury bonds within the available-for-sale securities portfolio, which are the result of changes in market interest rates since they were acquired.

About Oak View Bankshares, Inc. and Oak View National Bank

Oak View Bankshares, Inc. is the parent bank holding company for Oak View National Bank, a locally owned and managed community bank serving Fauquier, Culpeper, Rappahannock, and surrounding Counties. For more information about Oak View Bankshares, Inc. and Oak View National Bank, please visit our website at www.oakviewbank.com. Member FDIC.

For additional information, contact Tammy Frazier, Executive Vice President & Chief Financial Officer, Oak View Bankshares, Inc., at 540-359-7155.

Cautionary Note Regarding Forward-Looking Statements

Any statements in this release about expectations, beliefs, plans, objectives, assumptions or future events or performance are not historical facts and are forward-looking statements. These statements are often, but not always, made through the use of words or phrases such as "may," "should," "could," "would," "predict," "potential," "believe," "likely," "expect," "anticipate," "seek," "estimate," "intend," "plan," "project" and similar expressions. Accordingly, these statements involve estimates, assumptions, and uncertainties, and actual results may differ materially from those expressed in such statements. The following factors could cause the Company's actual results to differ materially from those projected in the forward-looking statements made in this document: changes in assumptions underlying the establishment of allowances for credit losses, and other estimates; the risks of changes in interest rates on levels, composition and costs of deposits, loan demand, and the values and liquidity of loan collateral, securities, and interest sensitive assets and liabilities; the effects of future economic, business and market conditions; legislative and regulatory changes, including changes in banking, securities, and tax laws and regulations and their application by our regulators; the Company's ability to maintain adequate liquidity by retaining deposit customers and secondary funding sources, especially if the Company's or banking industry's reputation becomes damaged; computer systems and infrastructure may be vulnerable to attacks by hackers or breached due to employee error, malfeasance, or other disruptions despite security measures implemented by the Company; risks inherent in making loans, such as repayment risks and fluctuating collateral values; governmental monetary and fiscal policies; changes in accounting policies, rules and practices; competition with other banks and financial institutions, and companies outside of the banking industry, including companies that have substantially greater access to capital and other resources; demand, development and acceptance of new products and services; problems with technology utilized by the Company; changing trends in customer profiles and behavior; success of acquisitions and operating initiatives, changes in business strategy or development of plans, and management of growth; reliance on senior management, including the ability to attract and retain key personnel; and inadequate design or circumvention of disclosure controls and procedures or internal controls. These factors could cause actual results or outcomes to differ materially from those expressed in any forward-looking statements made by the Company, and you should not place undue reliance on any such forward-looking statements. Any forward-looking statement speaks only as of the date on which it is made and the Company does not undertake any obligation to update any forward-looking statement or statements to reflect events or circumstances after the date on which such statement is made or to reflect the occurrence of unanticipated events. New factors emerge from time to time, and it is not possible for the Company to predict which will arise. In addition, the Company cannot assess the impact of each factor on the Company's business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements.

SOURCE: Oak View Bankshares, Inc.

View the original press release on ACCESS Newswire

K.Hill--AT