Trinity Bank Reports 1st Quarter Earnings up 7.8%

Trump earned over $1 bn from crypto ventures in 2025

Trump earned over $1 bn from crypto ventures in 2025

The Afghan women farmers keeping their village alive

The Afghan women farmers keeping their village alive

Asian stocks fluctuate as traders eye crucial US jobs data

Asian stocks fluctuate as traders eye crucial US jobs data

Madison Square Garden: from Nazis to Knicks, and now... Taylor's wedding?

Madison Square Garden: from Nazis to Knicks, and now... Taylor's wedding?

'Love it': Wimbledon's military stewards tradition turns 80

'Love it': Wimbledon's military stewards tradition turns 80

Venezuela quake survivors cherish kindness of strangers

Venezuela quake survivors cherish kindness of strangers

US deports first migrant to Pacific nation Palau

US deports first migrant to Pacific nation Palau

Potter admits Sweden couldn't live with France in World Cup defeat

Potter admits Sweden couldn't live with France in World Cup defeat

US coach dismisses European jinx ahead of Bosnia clash

US coach dismisses European jinx ahead of Bosnia clash

World Bank to phase out lending to China by 2031

World Bank to phase out lending to China by 2031

Mbappe scores twice as France breeze past Sweden into World Cup last 16

Mbappe scores twice as France breeze past Sweden into World Cup last 16

No corn dogs? Trump's 'Great American State Fair' threatens to be a flop

No corn dogs? Trump's 'Great American State Fair' threatens to be a flop

Haaland hailed as 'greatest' after more World Cup heroics

Haaland hailed as 'greatest' after more World Cup heroics

Koeman steps down as Netherlands coach after World Cup exit

Koeman steps down as Netherlands coach after World Cup exit

Nasdaq ends best quarter in 6 years as yen extends drop against dollar

Nasdaq ends best quarter in 6 years as yen extends drop against dollar

Zverev says Wimbledon hopes 'about me' despite open draw

Zverev says Wimbledon hopes 'about me' despite open draw

Lionel Scaloni: Argentina's mastermind marks 100 games in charge

Lionel Scaloni: Argentina's mastermind marks 100 games in charge

Mourinho's Real Madrid host Real Sociedad in La Liga opener

Mourinho's Real Madrid host Real Sociedad in La Liga opener

Football brings joy to Venezuelan kids displaced by quakes

Football brings joy to Venezuelan kids displaced by quakes

Haaland fires Norway into last 16 as France, Mexico look to advance

Haaland fires Norway into last 16 as France, Mexico look to advance

Merkel unveils official portrait for German chancellery

Merkel unveils official portrait for German chancellery

Canada crews battle northern wildfire after crash kills 3

Canada crews battle northern wildfire after crash kills 3

Portugal's Silva bides his time after being benched at World Cup

Portugal's Silva bides his time after being benched at World Cup

US stars relish soccer's primetime moment against Bosnia

US stars relish soccer's primetime moment against Bosnia

Lampard extends Coventry stay after promotion to Premier League

Lampard extends Coventry stay after promotion to Premier League

FORT WORTH, TX / ACCESS Newswire / May 5, 2025 / Trinity Bank N.A. (OTC PINK:TYBT) today announced operating results for the three months ending March 31, 2025.

Results of Operations

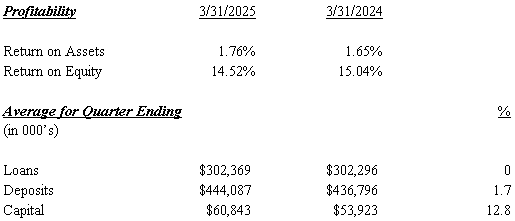

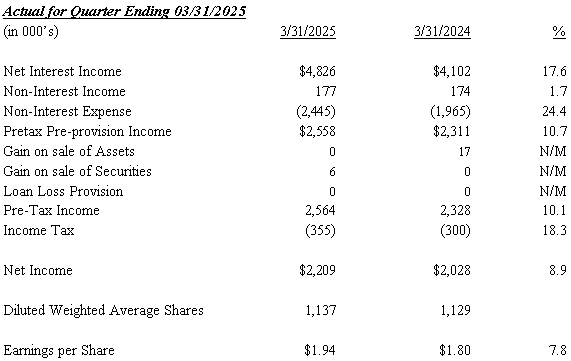

Trinity Bank, N.A. reported Net Income after Taxes of $2,209,000 or $1.94 per diluted common share for the first quarter of 2025, compared to $2,028,000 or $1.80 per diluted common share for the first quarter of 2024, an increase of 7.8%.

CEO Matt R. Opitz remarked, "We are pleased with the results of the 1 st Quarter. While loans remained flat, we have experienced an increase in requests for new loans as well as return on assets. This has been a mix of activity from existing customers as well as new customers to the bank. We have also experienced an increase in deposits which has continued into the 2 nd quarter.

Although these results mark our single best quarter since inception, we are aware of and focused on the economic volatility which is being driven primarily by the current tariff war and continued unrest stemming from the Russia and Ukraine war. As always, we remain focused on asset quality, liquidity, and conservative underwriting practices."

"With the additions of Chief Lending Officer, Steve Lombardi and Chief Operating Officer, Todd Crookshank, we are already experiencing the sizable benefits of their contributions. We are excited about the roles they will play in Trinity Bank moving forward."

Trinity announced its 27 th consecutive increase in its semiannual dividend. The dividend was paid this last week to shareholders. The April 2025 dividend of $0.95 per share represents an increase of 8% over the April 2024 dividend of $0.88 per share."

Trinity Bank, N.A. is a commercial bank that began operations May 28, 2003. For a full financial statement or for monthly updates on deposit rates and liquidity position visit Trinity Bank's website: www.trinitybk.com. Regulatory reporting format is also available at www.fdic.gov.

###

For information contact:

Richard Burt

Executive Vice President

Trinity Bank

817-763-9966

This Press Release may contain certain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 regarding future financial conditions, results of operations and the Bank's business operations. Such forward-looking statements involve risks, uncertainties and assumptions, including, but not limited to, monetary policy and general economic conditions in Texas and the greater Dallas-Fort Worth metropolitan area, the risks of changes in interest rates on the level and composition of deposits, loan demand and the values of loan collateral, securities and interest rate protection agreements, the actions of competitors and customers, the success of the Bank in implementing its strategic plan, the failure of the assumptions underlying the reserves for loan losses and the estimations of values of collateral and various financial assets and liabilities, that the costs of technological changes are more difficult or expensive than anticipated, the effects of regulatory restrictions imposed on banks generally, any changes in fiscal, monetary or regulatory policies and other uncertainties as discussed in the Bank's Registration Statement on Form SB‑1 filed with the Office of the Comptroller of the Currency. Should one or more of these risks or uncertainties materialize, or should these underlying assumptions prove incorrect, actual outcomes may vary materially from outcomes expected or anticipated by the Bank. A forward-looking statement may include a statement of the assumptions or bases underlying the forward‑looking statement. The Bank believes it has chosen these assumptions or bases in good faith and that they are reasonable. However, the Bank cautions you that assumptions or bases almost always vary from actual results, and the differences between assumptions or bases and actual results can be material. The Bank undertakes no obligation to publicly update or otherwise revise any forward‑looking statements, whether as a result of new information, future events or otherwise, unless the securities laws require the Bank to do so.

TRINITY BANK N.A.

(Unaudited)

(Dollars in thousands, except per share data)

Quarter Ended | ||||||||||

March 31 | % | |||||||||

EARNINGS SUMMARY | 2025 | 2024 | Change | |||||||

Interest income | $ | 6,975 | $ | 6,934 | 0.6 | % | ||||

Interest expense | 2,149 | 2,832 | -24.1 | % | ||||||

Net Interest Income | 4,826 | 4,102 | 17.6 | % | ||||||

Service charges on deposits | 71 | 53 | 34.0 | % | ||||||

Other income | 106 | 121 | -12.4 | % | ||||||

Total Non Interest Income | 177 | 174 | 1.7 | % | ||||||

Salaries and benefits expense | 1,508 | 1,223 | 23.3 | % | ||||||

Occupancy and equipment expense | 123 | 122 | 0.8 | % | ||||||

Other expense | 814 | 620 | 31.3 | % | ||||||

Total Non Interest Expense | 2,445 | 1,965 | 24.4 | % | ||||||

Pretax pre-provision income | 2,558 | 2,311 | 10.7 | % | ||||||

Gain on sale of Securities | 6 | 0 | N/M | |||||||

Gain on sale of Assets | 0 | 17 | N/M | |||||||

Provision for Loan Losses | 0 | 0 | N/M | |||||||

Earnings before income taxes | 2,564 | 2,328 | 10.1 | % | ||||||

Provision for income taxes | 355 | 300 | 18.3 | % | ||||||

Net Earnings | $ | 2,209 | $ | 2,028 | 8.9 | % | ||||

Basic earnings per share | 2.03 | 1.88 | 2.5 | % | ||||||

Basic weighted average shares | 1087 | 1,079 | ||||||||

outstanding | ||||||||||

Diluted earnings per share - estimate | 1.94 | 1.80 | 7.8 | % | ||||||

Diluted weighted average shares outstanding | 1,137 | 1,129 | ||||||||

Average for Quarter | ||||||||||

March 31 | % | |||||||||

BALANCE SHEET SUMMARY | 2025 | 2024 | Change | |||||||

Total loans | $ | 302,369 | $ | 302,296 | 0.0 | % | ||||

Total short term investments | 53,950 | 37,648 | 43.3 | % | ||||||

FRB Stock | 449 | 433 | 3.7 | % | ||||||

Total investment securities | 136,314 | 143,056 | -4.7 | % | ||||||

Earning assets | 493,082 | 483,001 | 2.1 | % | ||||||

Total assets | 503,366 | 490,262 | 2.7 | % | ||||||

Noninterest bearing deposits | 133,982 | 127,766 | 4.9 | % | ||||||

Interest bearing deposits | 310,105 | 309,030 | 0.3 | % | ||||||

Total deposits | 444,087 | 436,796 | 1.7 | % | ||||||

Fed Funds Purchased and Repurchase Agreements | 0 | 0 | N/M | |||||||

Shareholders' equity | $ | 60,843 | $ | 53,923 | 12.8 | % | ||||

TRINITY BANK N.A.

(Unaudited)

(Dollars in thousands, except per share data)

Average for Quarter Ending | ||||||||||||||||||

March 31, | Dec 31, | Sep 30, | June 30, | March 31, | ||||||||||||||

BALANCE SHEET SUMMARY | 2025 | 2024 | 2024 | 2024 | 2024 | |||||||||||||

Total loans | $ | 302,369 | $ | 297,595 | $ | 300,487 | $ | 306,551 | $ | 302,296 | ||||||||

Total short term investments | 53,950 | 84,667 | 38,112 | 25,626 | 37,649 | |||||||||||||

FRB Stock | 449 | 438 | 437 | 435 | 433 | |||||||||||||

Total investment securities | 136,314 | 139,200 | 137,751 | 137,088 | 142,623 | |||||||||||||

Earning assets | 493,082 | 521,900 | 476,787 | 469,700 | 483,001 | |||||||||||||

Total assets | 503,366 | 529,766 | 485,034 | 477,700 | 490,262 | |||||||||||||

Noninterest bearing deposits | 133,982 | 140,237 | 131,659 | 131,609 | 127,766 | |||||||||||||

Interest bearing deposits | 310,105 | 331,293 | 297,480 | 293,548 | 309,030 | |||||||||||||

Total deposits | 444,087 | 471,529 | 429,139 | 425,157 | 436,796 | |||||||||||||

Fed Funds Purchased and Repurchase Agreements | 0 | 0 | 0 | 0 | 0 | |||||||||||||

Shareholders' equity | $ | 60,843 | $ | 58,388 | $ | 56,857 | $ | 54,951 | $ | 53,923 | ||||||||

Quarter Ended | ||||||||||||||||||

March 31, | Dec 31, | Sep 30, | June 30, | March 31, | ||||||||||||||

HISTORICAL EARNINGS SUMMARY | 2025 | 2024 | 2024 | 2024 | 2024 | |||||||||||||

Interest income | $ | 6,975 | $ | 7,426 | $ | 7,112 | $ | 7,107 | $ | 6,934 | ||||||||

Interest expense | 2,149 | 2,681 | 2,749 | 2,713 | 2,832 | |||||||||||||

Net Interest Income | 4,826 | 4,745 | 4,363 | 4,394 | 4,102 | |||||||||||||

Service charges on deposits | 71 | 70 | 65 | 64 | 53 | |||||||||||||

Other income | 106 | 112 | 109 | 121 | 121 | |||||||||||||

Total Non Interest Income | 177 | 182 | 174 | 185 | 174 | |||||||||||||

Salaries and benefits expense | 1,508 | 1,343 | 1,368 | 1,319 | 1,223 | |||||||||||||

Occupancy and equipment expense | 123 | 117 | 133 | 122 | 122 | |||||||||||||

Other expense | 814 | 575 | 601 | 657 | 620 | |||||||||||||

Total Non Interest Expense | 2,445 | 2,035 | 2,102 | 2,098 | 1,965 | |||||||||||||

Pretax pre-provision income | 2,558 | 2,892 | 2,435 | 2,481 | 2,311 | |||||||||||||

Gain on sale of securities | 6 | 1 | 4 | (4 | ) | 0 | ||||||||||||

Gain on sale of Other Assets | 0 | 0 | 0 | 36 | 17 | |||||||||||||

Provision for Loan Losses | 0 | 350 | 0 | 0 | 0 | |||||||||||||

Earnings before income taxes | 2,564 | 2,543 | 2,439 | 2,514 | 2,328 | |||||||||||||

Provision for income taxes | 355 | 365 | 340 | 360 | 300 | |||||||||||||

Net Earnings | $ | 2,209 | $ | 2,178 | $ | 2,099 | $ | 2,154 | $ | 2,028 | ||||||||

Diluted earnings per share | $ | 1.94 | $ | 1.92 | $ | 1.86 | $ | 1.91 | $ | 1.80 | ||||||||

TRINITY BANK N.A.

(Unaudited)

(Dollars in thousands, except per share data)

Ending Balance | ||||||||||||||||||

March 31, | Dec. 31, | Sept. 30, | June 30, | March 31, | ||||||||||||||

HISTORICAL BALANCE SHEET | 2025 | 2024 | 2024 | 2024 | 2024 | |||||||||||||

Total loans | $ | 304,944 | $ | 305,864 | $ | 296,906 | $ | 304,810 | $ | 312,372 | ||||||||

FRB Stock | 456 | 439 | 438 | 435 | 435 | |||||||||||||

Total short term investments | 90,040 | 69,746 | 59,576 | 10,003 | 38,009 | |||||||||||||

Total investment securities | 124,619 | 138,306 | 137,510 | 136,331 | 139,598 | |||||||||||||

Total earning assets | 520,059 | 514,355 | 494,430 | 451,579 | 490,414 | |||||||||||||

Allowance for loan losses | (5,586 | ) | (5,583 | ) | (5,230 | ) | (5,227 | ) | (5,225 | ) | ||||||||

Premises and equipment | 4,044 | 4,123 | 2,393 | 2,397 | 2,375 | |||||||||||||

Other Assets | 10,297 | 9,339 | 9,739 | 14,276 | 7,714 | |||||||||||||

Total assets | 528,814 | 522,234 | 501,332 | 463,025 | 495,278 | |||||||||||||

Noninterest bearing deposits | 140,500 | 146,834 | 137,594 | 128,318 | 130,876 | |||||||||||||

Interest bearing deposits | 329,329 | 318,206 | 305,010 | 280,945 | 310,889 | |||||||||||||

Total deposits | 469,829 | 465,040 | 442,604 | 409,263 | 441,765 | |||||||||||||

Fed Funds Purchased and Repurchase Agreements | 0 | 0 | 0 | 0 | 0 | |||||||||||||

Other Liabilities | 2,661 | 2,711 | 2,901 | 2,804 | 2,618 | |||||||||||||

Total liabilities | 472,490 | 467,751 | 445,505 | 412,067 | 444,383 | |||||||||||||

Shareholders' Equity Actual | 62,276 | 59,758 | 57,976 | 55,915 | 54,777 | |||||||||||||

Unrealized Gain/Loss - AFS | (5,952 | ) | (5,275 | ) | (2,149 | ) | (4,957 | ) | (3,883 | ) | ||||||||

Total Equity | $ | 56,324 | $ | 54,483 | $ | 55,827 | $ | 50,958 | $ | 50,894 | ||||||||

Quarter Ending | ||||||||||||||||||

March 31, | Dec. 31, | Sept. 30, | June 30, | March 31, | ||||||||||||||

NONPERFORMING ASSETS | 2025 | 2024 | 2024 | 2024 | 2024 | |||||||||||||

Nonaccrual loans | $ | 949 | $ | 1,047 | $ | 0 | $ | 0 | $ | 0 | ||||||||

Restructured loans | 0 | 0 | 505 | 552 | 598 | |||||||||||||

Other real estate & foreclosed assets | 0 | 0 | 0 | 0 | 0 | |||||||||||||

Accruing loans past due 90 days or more | 0 | 0 | 0 | 0 | 0 | |||||||||||||

Total nonperforming assets | $ | 949 | $ | 1,047 | $ | 505 | $ | 552 | $ | 598 | ||||||||

Accruing loans past due 30-89 days | $ | 1,000 | $ | 0 | $ | 39 | $ | 1,274 | $ | 0 | ||||||||

Total nonperforming assets as a percentage | ||||||||||||||||||

of loans and foreclosed assets | 0.31 | % | 0.34 | % | 0.17 | % | 0.18 | % | 0.19 | % | ||||||||

TRINITY BANK N.A.

(Unaudited)

(Dollars in thousands, except per share data)

Quarter Ending | |||||||||||||||||||

ALLOWANCE FOR | March 31, | Dec. 31, | Sept. 30, | June 30, | March 31, | ||||||||||||||

LOAN LOSSES | 2025 | 2024 | 2024 | 2024 | 2024 | ||||||||||||||

Balance at beginning of period | $ | 5,583 | $ | 5,230 | $ | 5,227 | $ | 5,224 | $ | 5,224 | |||||||||

Loans charged off | 0 | 0 | 0 | 0 | 0 | ||||||||||||||

Loan recoveries | 3 | 3 | 3 | 3 | 0 | ||||||||||||||

Net (charge-offs) recoveries | 3 | 3 | 3 | 3 | 0 | ||||||||||||||

Provision for loan losses | 0 | 350 | 0 | 0 | 0 | ||||||||||||||

Balance at end of period | $ | 5,586 | $ | 5,583 | $ | 5,230 | $ | 5,227 | $ | 5,224 | |||||||||

Allowance for loan losses | |||||||||||||||||||

as a percentage of total loans | 1.83 | % | 1.83 | % | 1.76 | % | 1.71 | % | 1.67 | % | |||||||||

Allowance for loan losses | |||||||||||||||||||

as a percentage of nonperforming assets | 589 | % | 533 | % | 1036 | % | 947 | % | 874 | % | |||||||||

Net charge-offs (recoveries) as a | |||||||||||||||||||

percentage of average loans | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | |||||||||

Provision for loan losses | |||||||||||||||||||

as a percentage of average loans | 0.00 | % | 0.11 | % | 0.00 | % | 0.00 | % | 0.00 | % | |||||||||

Quarter Ending | |||||||||||||||||||

March 31, | Dec. 31, | Sept. 30, | June 30, | ||||||||||||||||

SELECTED RATIOS | 2025 | 2024 | 2024 | 2024 | 2024 | ||||||||||||||

Return on average assets (annualized) | 1.76 | % | 1.64 | % | 1.73 | % | 1.80 | % | 1.65 | % | |||||||||

Return on average equity (annualized) | 15.67 | % | 15.85 | % | 15.91 | % | 17.42 | % | 16.03 | % | |||||||||

Return on average equity (excluding unrealized gain on investments) | 14.52 | % | 14.92 | % | 14.77 | % | 15.68 | % | 15.04 | % | |||||||||

Average shareholders' equity to average assets | 12.09 | % | 11.02 | % | 11.72 | % | 11.50 | % | 11.00 | % | |||||||||

Yield on earning assets (tax equivalent) | 5.72 | % | 5.92 | % | 6.20 | % | 6.28 | % | 5.97 | % | |||||||||

Effective Cost of Funds | 1.75 | % | 2.06 | % | 2.31 | % | 2.31 | % | 2.34 | % | |||||||||

Net interest margin (tax equivalent) | 3.97 | % | 3.86 | % | 3.89 | % | 3.97 | % | 3.63 | % | |||||||||

Efficiency ratio (tax equivalent) | 46.2 | % | 39.0 | % | 43.7 | % | 43.2 | % | 43.1 | % | |||||||||

End of period book value per common share | $ | 51.82 | $ | 50.21 | $ | 51.79 | $ | 47.23 | $ | 47.17 | |||||||||

End of period book value (excluding unrealized gain/loss on investments) | $ | 57.29 | $ | 55.08 | $ | 53.78 | $ | 51.82 | $ | 50.77 | |||||||||

End of period common shares outstanding (in 000's) | 1,087 | 1,085 | 1,078 | 1,079 | 1,079 | ||||||||||||||

TRINITY BANK N.A.

(Unaudited)

(Dollars in thousands, except per share data)

Three Months Ending | ||||||||||||||||||||||||||||||

March 31, 2025 | March 31, 2024 | |||||||||||||||||||||||||||||

Tax | Tax | |||||||||||||||||||||||||||||

Average | Equivalent | Average | Equivalent | |||||||||||||||||||||||||||

YIELD ANALYSIS | Balance | Interest | Yield | Yield | Balance | Interest | Yield | Yield | ||||||||||||||||||||||

Interest Earning Assets: | ||||||||||||||||||||||||||||||

Short term investment | $ | 53,950 | $ | 606 | 4.49 | % | 4.49 | % | $ | 37,649 | $ | 517 | 5.49 | % | 5.49 | % | ||||||||||||||

FRB Stock | 449 | 7 | 6.00 | % | 6.00 | % | 433 | 6 | 6.00 | % | 6.00 | % | ||||||||||||||||||

Taxable securities | 1,755 | 21 | 4.79 | % | 4.79 | % | 2,472 | 32 | 5.18 | % | 5.18 | % | ||||||||||||||||||

Tax Free securities | 134,560 | 1,107 | 3.29 | % | 3.51 | % | 140,151 | 1,047 | 2.99 | % | 3.78 | % | ||||||||||||||||||

Loans | 302,369 | 5,234 | 6.92 | % | 6.92 | % | 302,296 | 5,331 | 7.05 | % | 7.05 | % | ||||||||||||||||||

Total Interest Earning Assets | 493,083 | 6,975 | 5.66 | % | 5.72 | % | 483,001 | 6,933 | 5.74 | % | 5.97 | % | ||||||||||||||||||

Noninterest Earning Assets: | ||||||||||||||||||||||||||||||

Cash and due from banks | 6,614 | 5,427 | ||||||||||||||||||||||||||||

Other assets | 9,254 | 7,059 | ||||||||||||||||||||||||||||

Allowance for loan losses | (5,585 | ) | (5,225 | ) | ||||||||||||||||||||||||||

Total Noninterest Earning Assets | 10,283 | 7,261 | ||||||||||||||||||||||||||||

Total Assets | $ | 503,366 | $ | 490,262 | ||||||||||||||||||||||||||

Interest Bearing Liabilities: | ||||||||||||||||||||||||||||||

Transaction and Money Market accounts | $ | 198,760 | $ | 1,055 | 2.12 | % | 2.12 | % | 204,700 | $ | 1,141 | 2.23 | % | 2.23 | % | |||||||||||||||

Certificates and other time deposits | 111,345 | 1,094 | 3.93 | % | 3.93 | % | 95,663 | 1,678 | 7.02 | % | 7.02 | % | ||||||||||||||||||

Other borrowings | 0 | 0 | 0.00 | % | 0.00 | % | 8,667 | 13 | 0.60 | % | 0.60 | % | ||||||||||||||||||

Total Interest Bearing Liabilities | 310,105 | 2,149 | 2.77 | % | 2.87 | % | 309,030 | 2,832 | 3.67 | % | 3.67 | % | ||||||||||||||||||

Noninterest Bearing Liabilities: | ||||||||||||||||||||||||||||||

Demand deposits | 133,982 | 127,766 | ||||||||||||||||||||||||||||

Other liabilities | 2,887 | 2,856 | ||||||||||||||||||||||||||||

Shareholders' Equity | 56,392 | 50,610 | ||||||||||||||||||||||||||||

Total Liabilities and Shareholders Equity | $ | 503,366 | $ | 490,262 | ||||||||||||||||||||||||||

Net Interest Income and Spread | $ | 182,978 | $ | 4,826 | 2.89 | % | 2.85 | % | 173,971 | $ | 4,101 | 2.08 | % | 2.31 | % | |||||||||||||||

Net Interest Margin | 3.91 | % | 3.97 | % | 3.40 | % | 3.63 | % | ||||||||||||||||||||||

TRINITY BANK N.A.

(Unaudited)

(Dollars in thousands, except per share data)

March 31 | March 31 | |||||||

2025 | % | 2024 | % | |||||

LOAN PORTFOLIO | ||||||||

Commercial and industrial | $ | 164,244 | 53.86 | % | $ | 171,356 | 54.86 | % |

Real estate: | ||||||||

Commercial | 97,115 | 31.85 | % | 95,893 | 30.70 | % | ||

Residential | 9,859 | 3.23 | % | 15,877 | 5.08 | % | ||

Construction and development | 33,414 | 10.96 | % | 28,974 | 9.28 | % | ||

Consumer | 312 | 0.10 | % | 272 | 0.09 | % | ||

Total loans | $ | 304,944 | 100.00 | % | 312,372 | 100.00 | % | |

March 31 | March 31 | |||||||

2025 | 2024 | |||||||

REGULATORY CAPITAL DATA | ||||||||

Tier 1 Capital | $ | 62,276 | $ | 54,777 | ||||

Total Capital (Tier 1 + Tier 2) | $ | 66,622 | $ | 59,197 | ||||

Total Risk-Adjusted Assets | $ | 346,179 | $ | 352,550 | ||||

Tier 1 Risk-Based Capital Ratio | 17.99 | % | 15.54 | % | ||||

Total Risk-Based Capital Ratio | 19.25 | % | 16.79 | % | ||||

Tier 1 Leverage Ratio | 12.37 | % | 11.17 | % | ||||

OTHER DATA | ||||||||

Full Time Equivalent | ||||||||

Employees (FTE's) | 31 | 28 | ||||||

Stock Price Range | ||||||||

(For the Three Months Ended): | ||||||||

High | $ | 91.00 | $ | 95.00 | ||||

Low | $ | 84.00 | $ | 89.00 | ||||

Close | $ | 85.00 | $ | 94.00 | ||||

SOURCE: Trinity Bank, NA (Fort Worth, Texas)

View the original press release on ACCESS Newswire

M.King--AT