Turkey halts four-month streak of rate cuts

Barred from elections, Russia's anti-war party vows to fight on

Barred from elections, Russia's anti-war party vows to fight on

Jaissle states Newcastle ambition but urges patience

Jaissle states Newcastle ambition but urges patience

NBA star Cooper Flagg trading card a slam dunk for lucky buyer

NBA star Cooper Flagg trading card a slam dunk for lucky buyer

ForumPay Expands Payment Infrastructure with New Card and Bank Transfer Acceptance Solution

ForumPay Expands Payment Infrastructure with New Card and Bank Transfer Acceptance Solution

Oil prices higher, stocks flat ahead of inflation report

Oil prices higher, stocks flat ahead of inflation report

Orban-critic ex-judge becomes Hungary president after predecessor ouster

Orban-critic ex-judge becomes Hungary president after predecessor ouster

US rights groups sue Trump over ICC sanctions

US rights groups sue Trump over ICC sanctions

Sphere 3D Corp. (Nasdaq: ANY) Attracts 6.5% Stake from Turnaround Bitcoin-Mining Investor

Sphere 3D Corp. (Nasdaq: ANY) Attracts 6.5% Stake from Turnaround Bitcoin-Mining Investor

Oil prices lower, stocks higher as Hormuz doubts drag on

Oil prices lower, stocks higher as Hormuz doubts drag on

Colombia scrambles to find survivors as quake kills 181

Colombia scrambles to find survivors as quake kills 181

Colombia scrambles to find survivors as quake kills 169

Colombia scrambles to find survivors as quake kills 169

MEXC Report: 74.2% of Traditional Finance Users Have Shifted Their Trading Activity to Crypto Exchanges

MEXC Report: 74.2% of Traditional Finance Users Have Shifted Their Trading Activity to Crypto Exchanges

MEXC Lists DAPPOS (DOS) With $60,000 Worth of DOS and 10,000 USDT in Airdrop+ Rewards

MEXC Lists DAPPOS (DOS) With $60,000 Worth of DOS and 10,000 USDT in Airdrop+ Rewards

Jellyfish force shutdown of three reactors at French nuclear plant

Jellyfish force shutdown of three reactors at French nuclear plant

Hodgkinson, Werro sail through Euro 800m qualifying

Hodgkinson, Werro sail through Euro 800m qualifying

Somali referee denied World Cup 'proud' to oversee UEFA Super Cup

Somali referee denied World Cup 'proud' to oversee UEFA Super Cup

French newspapers target Google over AI summaries

French newspapers target Google over AI summaries

Ebola death toll in DR Congo outbreak rises to more than 2,000

Ebola death toll in DR Congo outbreak rises to more than 2,000

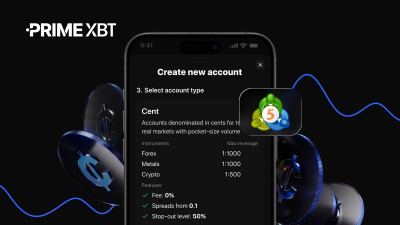

PrimeXBT Launches MT5 Cent Account for Beginners and Risk-Conscious Traders

PrimeXBT Launches MT5 Cent Account for Beginners and Risk-Conscious Traders

British sprinter Hunt chasing three more golds after winning 100m

British sprinter Hunt chasing three more golds after winning 100m

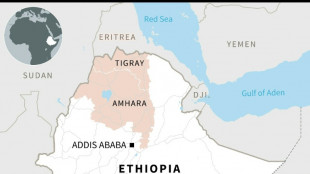

Ethiopia's Tigray rebel authorities condemn army drone strikes

Ethiopia's Tigray rebel authorities condemn army drone strikes

Too hot to live? French buyers rethink housing choices after heatwaves

Too hot to live? French buyers rethink housing choices after heatwaves

Ukraine says Russia fired N. Korean missiles in deadly attack

Ukraine says Russia fired N. Korean missiles in deadly attack

Oil prices jump further as hopes for Hormuz deal fade

Oil prices jump further as hopes for Hormuz deal fade

Trump says would be 'terrible mistake' to oust embattled Infantino

Trump says would be 'terrible mistake' to oust embattled Infantino

Turkey's central bank on Thursday bowed to market pressure and halted a four-month streak of interest rate cuts that saw inflation soar and the currency collapse.

The bank left its policy rate at 14 percent two days after President Recep Tayyip Erdogan -- a fervent opponent of high interest rates -- said future reductions could come "gradually and without any rush".

Erdogan has been waging a "war of economic independence" designed to break Turkey's dependence on foreign currency inflows by boosting cheap lending and revving up exports.

But the policies have seen the emerging country's economy spin dangerously out of control.

Turkey's annual inflation rate has shot to a 19-year high of 36 percent and is expected to keep climbing.

The lira lost 44 percent of its value against the dollar and became the world's worst-performing emerging market currency last year.

And the central bank's net reserves -- a gauge of both Turkey's economic health and ability to withstand a potential banking crisis -- have dropped from $21.1 billion (18.6 billion euros) in mid-December to $7.9 billion on January 7.

"The sharp falls in the lira risk entrenching inflation at very high levels," Jason Tuvey of Capital Economics said in a note to clients.

"And the weak lira could cause vulnerabilities in the banking sector to crystallise."

- 'Bad policy for longer' -

Erdogan has cited Islamic rules against usury to justify his belief that high interest rates cause inflation. Economists almost universally agree that the opposite is true.

Central banks hike rates in order to raise the cost of doing business when the economy is growing too fast. This helps bring down prices by reducing demand.

High rates also help support currencies by raising the return on local bank deposits and investments.

But Erdogan says Turkey has developed a "new economic model" for achieving sustainable growth.

The central bank attributed the spike in inflation from 21.3 percent in November to 36.2 percent last month to "distorted pricing behaviour (caused by) unhealthy price formations in the foreign exchange market".

It also blamed outside factors such as high commodity prices and global supply chain bottlenecks caused by the coronavirus pandemic.

The lira edged up slightly after the announcement to around 13.3 to the dollar.

Economists believe the bank would need to hike its policy rate substantially in order to solve Turkey's accumulating problems.

"No change (means) bad policy for longer," emerging markets economist Timothy Ash of BlueBay Asset Management remarked after the rate decision.

- 'Lira is our money'

Turks had been converting their liras into gold and dollars in order to shield themselves from price increases and an erosion of their purchasing power.

The government has tried to stem this tide by creating new bank deposits that effectively tie the value of the lira to the dollar.

Erdogan says the new scheme has attracted 163 billion liras ($12.2 billion).

He has also appealed on Turks' sense of patriotism while urging them to hold on to their liras.

"The Turkish lira is our money," he said in a traditional New Year's Eve address. "That is how we move forward -- not with this or that currency."

Yet fresh data released on Thursday showed that 62.2 percent of all Turks' deposits were still held in dollars.

The figure was down by just 1.4 percentage points on the week.

Economists believe that the mechanism is having only a marginal effect because it forces individuals and businesses to hold liras in the new deposits for at least three months.

Exporters are also unhappy with a new requirement to sell a quarter of their hard currency proceeds to the central bank.

P.A.Mendoza--AT