Commencement Bancorp, Inc. (CBWA) Announces Third Quarter 2025 Results

France, Germany reach deal on arms maker KNDS, paving way for IPO

France, Germany reach deal on arms maker KNDS, paving way for IPO

France set for hottest day yet of heatwave

France set for hottest day yet of heatwave

Gaza's surfers seek solace in the sea

Gaza's surfers seek solace in the sea

EasyJet rejects £5 bn takeover offer from US equity firm

EasyJet rejects £5 bn takeover offer from US equity firm

Mediators hail 'progress' in US-Iran talks after lengthy opening session

Mediators hail 'progress' in US-Iran talks after lengthy opening session

Coffee break: Starbucks Korea stores pause for training after 'Tank Day' fiasco

Coffee break: Starbucks Korea stores pause for training after 'Tank Day' fiasco

Rare Philippine school shooting kills three teens, wounds seven

Rare Philippine school shooting kills three teens, wounds seven

Crude prices drop after 'positive' US-Iran talks

Crude prices drop after 'positive' US-Iran talks

Tuchel's England face defensive questions despite flying start at World Cup

Tuchel's England face defensive questions despite flying start at World Cup

Not just a hideout: Sahel forests provide base for jihadists

Not just a hideout: Sahel forests provide base for jihadists

Africa faces child surgery crisis as key anaesthesia runs out

Africa faces child surgery crisis as key anaesthesia runs out

J-Bay: S.Africa's surf mecca missing out on the global tour

J-Bay: S.Africa's surf mecca missing out on the global tour

Key points from the first round of Iran-US talks

Key points from the first round of Iran-US talks

Crude prices drop, most stocks rise on 'positive' US-Iran talks

Crude prices drop, most stocks rise on 'positive' US-Iran talks

Slimy beans: Japanese natto disgusts and delights the world

Slimy beans: Japanese natto disgusts and delights the world

Cape Verde targeting World Cup knockout rounds after Uruguay draw: coach

Cape Verde targeting World Cup knockout rounds after Uruguay draw: coach

New coach Rennie names Savea as All Blacks captain

New coach Rennie names Savea as All Blacks captain

Yamal kickstarts Spain World Cup bid as Cape Verde stun Uruguay

Yamal kickstarts Spain World Cup bid as Cape Verde stun Uruguay

Introduces POS Ready for FWA12 to Help Retailers and Restaurants Protect Payment Traffic

Introduces POS Ready for FWA12 to Help Retailers and Restaurants Protect Payment Traffic

InterContinental Hotels Group PLC Announces Transaction in Own Shares - June 22

InterContinental Hotels Group PLC Announces Transaction in Own Shares - June 22

Guardian Metal Resources PLC Announces Holding(s) in Company

Guardian Metal Resources PLC Announces Holding(s) in Company

Apex Drills 14.9 m of 5.09 % REO and 12.3 m of 5.63 % REO with > 2.50 % REO Intercept Over 191.9 m in the Trinity Zone at the Rift Rare Earth Project

Apex Drills 14.9 m of 5.09 % REO and 12.3 m of 5.63 % REO with > 2.50 % REO Intercept Over 191.9 m in the Trinity Zone at the Rift Rare Earth Project

CTT Pharma Signs LOI for Clinical Trials and Testing of Nicotine Products

CTT Pharma Signs LOI for Clinical Trials and Testing of Nicotine Products

Who is the Best Plastic Surgeon for Skin Removal After Weight Loss?

Who is the Best Plastic Surgeon for Skin Removal After Weight Loss?

Mexican fans rally behind Iran as 'our second team' at World Cup

Mexican fans rally behind Iran as 'our second team' at World Cup

2025 Third Quarter Financial Highlights:

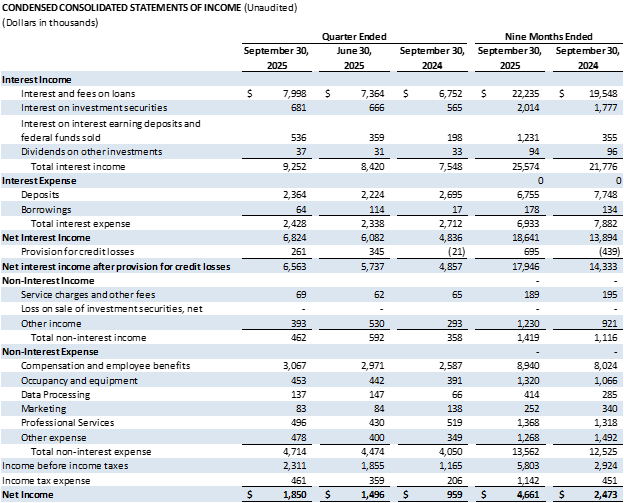

Net income was $1.9 million compared to $1.5 million for the second quarter of 2025 and $1.0 million for the third quarter of 2024.

Strong year-to-date loan growth of 9.6%.

Deposits increased $6.1 million, or 4.0% annualized growth rate.

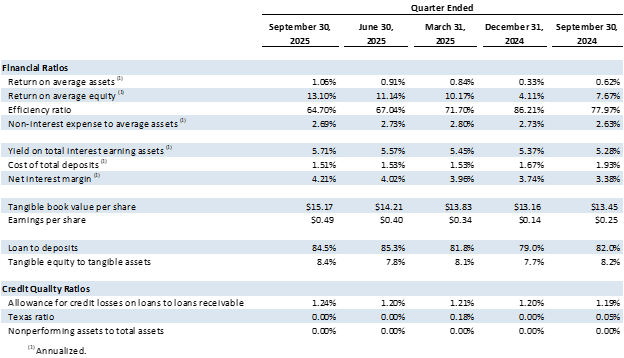

Net interest margin increased to 4.21% from 4.02% during the second quarter of 2025.

Total cost of deposits decreased to 1.51% from 1.53% during the second quarter of 2025.

The Bank had no nonperforming assets as of September 30, 2025.

Capital ratios remained well above regulatory requirements.

TACOMA, WA / ACCESS Newswire / October 30, 2025 / Commencement Bancorp, Inc. (OTCQX:CBWA) (the "Company", "we," or "us"), the parent company of Commencement Bank (the "Bank") reported net income of $1.9 million, or $0.49 per share, for the third quarter of 2025, compared to $1.5 million, or $0.40 per share, for the second quarter of 2025 and $1.0 million, or $0.25 per share, for the third quarter of 2024.

"We are very pleased with our third quarter operating results and the momentum we've sustained throughout the year. Our disciplined approach to managing deposit costs and loan yields, while strategically pursuing asset growth, is delivering tangible results. This is reflected in our stable cost of funds and continued improvement in quarterly profitability. We believe our long-term focus will continue to drive meaningful shareholder value over time," said John E. Manolides, Chief Executive Officer.

"I'm appreciative of our bankers' continued business development activities across multiple business lines. The collaboration with Mary Bridge Children's Therapy Services Center is a highlight of our efforts this quarter. By supporting the creation of this new 16,000-square-foot children's outpatient therapy center, we are helping to build a stronger, healthier community for the future. We look forward to its grand opening in late 2026," stated Nigel L. English, President & Chief Operating Officer. "We continue to achieve strong margin expansion, marking this the sixth consecutive quarter of growth, with a net interest margin of 4.21% during the third quarter. We're grateful to our bankers, customers, and shareholders as we look forward to finishing out a successful year."

Balance Sheet

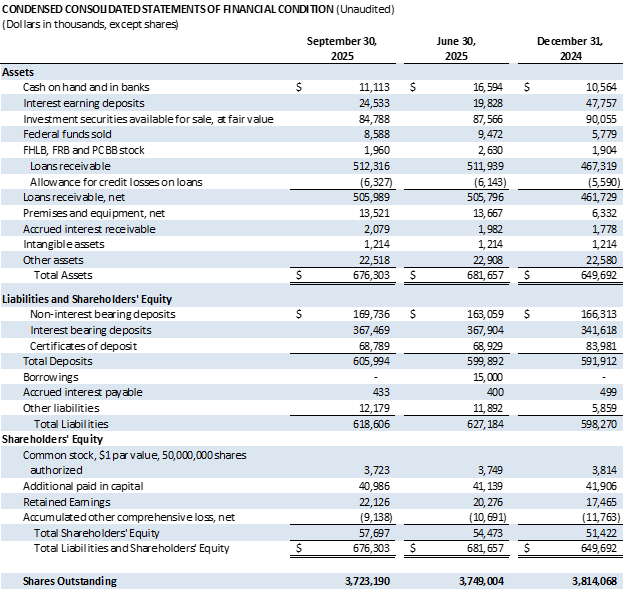

Total assets decreased $5.4 million to $676.3 million at September 30, 2025 from $681.7 million at June 30, 2025.

Investment securities available for sale decreased $2.8 million, or 3.2%, to $84.8 million at September 30, 2025 from $87.6 million at June 30, 2025. This decrease was due to principal payments and amortization of $4.8 million and a decrease in unrealized losses of $2.0 million. The decrease in market rates at September 30, 2025 caused the decrease in unrealized losses.

Loans receivable increased $0.4 million to $512.3 million at September 30, 2025 from $511.9 million at June 30, 2025 due primarily to an expected significant loan payoff of $6.8 million, offset by new loan originations. The Bank originated commitments of $43.0 million during third quarter of 2025 compared to $62.3 million during the second quarter of 2025 and $20.8 million during the third quarter of 2024.

Total deposits increased $6.1 million, or 1.0%, to $606.0 million at September 30, 2025 from $599.9 million at June 30, 2025. Noninterest bearing deposits, as a percentage of total deposits, increased to 28.0% at September 30, 2025.

The Company had no borrowings at September 30, 2025 compared to $15.0 million at June 30, 2025. The Company paid the 3-month advance from the Federal Home Loan Bank ("FHLB") in early August 2025.

Credit Quality

The Bank had no nonperforming assets at September 30, 2025 or June 30, 2025. The allowance for credit losses to loan receivable remains strong at 1.24% at September 30, 2025.

The percentage of classified loans (loans rated Substandard or worse) to loans receivable improved to 1.63% at September 30, 2025 from 1.67% at June 30, 2025 due primarily to principal payments and an upgrade of a consumer loan. The Bank proactively downgrades loans if the borrower is experiencing financial difficulties and upgrades loans if the borrower demonstrates sustained financial performance.

Liquidity

The Bank has ample liquidity with both on- and off-balance sheet sources. Total on-balance sheet liquidity of $127.5 million, or 18.9% of total assets at September 30, 2025, includes cash and cash equivalents as well as unencumbered investment securities. The Bank had access to available Federal Home Loan Bank advances, Federal Reserve discount window, and federal fund lines with correspondent banks of $220.5 million at September 30, 2025.

Income Statement

Net interest income increased $742,000, or 12.2%, during the third quarter of 2025 compared to the second quarter of 2025 due to the increase in interest income of $832,000, offset by the increase in interest expense of $90,000. Net interest margin increased 19 basis points ("bps") to 4.21% during the third quarter of 2025 from 4.02% during the second quarter of 2025 and increased 83 bps from 3.38% during the third quarter of 2024.

Interest income on loans increased $634,000 during the third quarter of 2025 compared to the second quarter of 2025 due primarily to an increase in average balance of loans of $22.8 million. The yield on net loans increased 16 bps to 6.28% for the third quarter of 2025 from 6.11% for the second quarter of 2025 due to loan mix, higher yields on new originations, and repricing higher on existing portfolio rates.

Interest expense on deposits increased $140,000 during the third quarter of 2025 compared to the second quarter of 2025 due to an increase in the average balance of interest bearing deposits of $24.4 million. Total cost of deposits was 1.51% for third quarter of 2025 compared to 1.53% for the second quarter of 2025. Average noninterest bearing demand deposits increased $14.5 million during the third quarter of 2025 and represent 28.0% of total deposits at September 30, 2025.

Interest expense on borrowings decreased $50,000 during the third quarter of 2025 due to the payoff of the FHLB advance of $15.0 million during the quarter. The cost of the short-term funding was augmented by dividends from the FHLB stock, of which a portion of the dividend is anticipated during fourth quarter of 2025.

Total non-interest income decreased $130,000 during the third quarter of 2025 compared to the second quarter of 2025 due to the recognition of loan swap fee income of $188,000 during the second quarter of 2025.

Total non-interest expense increased $240,000, or 5.4%, during the third quarter of 2025 compared to the second quarter of 2025 due primarily to an increase in compensation and employee benefits related to an increase in full-time equivalents and incentive compensation accrual.

###

About Commencement Bancorp, Inc.

Commencement Bancorp, Inc. is the holding company for Commencement Bank, headquartered in Tacoma, Washington. Commencement Bank was formed in 2006 to provide traditional, reliable, and sustainable banking in Pierce, King, Kitsap, and Thurston counties and the surrounding areas. Their team of experienced banking experts focuses on personal attention, flexible service, and building strong relationships with customers through state-of-the-art technology as well as traditional delivery systems. As a local bank, Commencement Bank is deeply committed to the community. For more information, please visit www.commencementbank.com. For information related to the trading of CBWA, please visit www.otcmarkets.com

For further discussion, please contact the following:

John E. Manolides,Chief Executive Officer | 253-284-1802

Nigel L. English, President & Chief Operating Officer | 253-284-1801

Brandi Parker, Executive Vice President & Chief Financial Officer | 253-284-1803

Forward-Looking Statement Safe Harbor: This news release contains comments or information that constitutes forward-looking statements (within the meaning of the Private Securities Litigation Reform Act of 1995) that are based on current expectations that involve a number of risks and uncertainties. Forward-looking statements describe Commencement Bancorp, Inc.'s projections, estimates, plans and expectations of future results and can be identified by words such as "believe," "intend," "estimate," "likely," "anticipate," "expect," "looking forward," and other similar expressions. They are not guarantees of future performance. Actual results may differ materially from the results expressed in these forward-looking statements, which because of their forward-looking nature, are difficult to predict. Investors should not place undue reliance on any forward-looking statement, and should consider factors that might cause differences including but not limited to the degree of competition by traditional and nontraditional competitors, declines in real estate markets, an increase in unemployment or sustained high levels of unemployment; changes in interest rates; greater than expected costs to integrate acquisitions, adverse changes in local, national and international economies; changes in the Federal Reserve's actions that affect monetary and fiscal policies; changes in legislative or regulatory actions or reform, including without limitation, the Dodd-Frank Wall Street Reform and Consumer Protection Act; demand for products and services; changes to the quality of the loan portfolio and our ability to succeed in our problem-asset resolution efforts; the impact of technological advances; changes in tax laws; and other risk factors. Commencement Bancorp, Inc.undertakes no obligation to publicly update or clarify any forward-looking statement to reflect the impact of events or circumstances that may arise after the date of this release.

SOURCE: Commencement Bank

View the original press release on ACCESS Newswire

M.O.Allen--AT