4 Ways to Calculate Your Life Insurance Coverage Needs in 2024

Trump orders new strikes on Iran over attacks on shipping in Hormuz

Trump orders new strikes on Iran over attacks on shipping in Hormuz

PSG's Lee set to join Atletico Madrid

PSG's Lee set to join Atletico Madrid

Iran plays with fire, but calculates Trump will hold back

Iran plays with fire, but calculates Trump will hold back

Oil surges, stocks slide as Trump says Iran ceasefire over

Oil surges, stocks slide as Trump says Iran ceasefire over

Meta to build $9 billion data center in western Canada

Meta to build $9 billion data center in western Canada

Rogers backs Kane to outshine Haaland in World Cup showdown

Rogers backs Kane to outshine Haaland in World Cup showdown

Some US Fed officials considered June rate hike on war fallout

Some US Fed officials considered June rate hike on war fallout

UN launches appeal for nearly $300 mn in Venezuela quake relief

UN launches appeal for nearly $300 mn in Venezuela quake relief

US to remove Syria from terror blacklist, in new boost to Sharaa

US to remove Syria from terror blacklist, in new boost to Sharaa

Court rejects Trump request to restore his name to Kennedy Center

Court rejects Trump request to restore his name to Kennedy Center

MLB pitching great Verlander to retire after 2026 season

MLB pitching great Verlander to retire after 2026 season

Artificial cloud brightening could tame El Nino, but with risks: study

Artificial cloud brightening could tame El Nino, but with risks: study

Shocked and shaken, Venezuela quake survivors get psychological help

Shocked and shaken, Venezuela quake survivors get psychological help

France, Morocco kick off blockbuster World Cup quarter-finals

France, Morocco kick off blockbuster World Cup quarter-finals

Amorim hails 'ambitious' AC Milan, promises to learn Italian

Amorim hails 'ambitious' AC Milan, promises to learn Italian

Cancer survivor Traeen takes the long road to Tour yellow

Cancer survivor Traeen takes the long road to Tour yellow

Easing Russian Olympic restrictions 'terrible', says Wimbledon star Kostyuk

Easing Russian Olympic restrictions 'terrible', says Wimbledon star Kostyuk

'Unbelievable' Kooij wins Tour de France 5th stage in chaotic sprint finish

'Unbelievable' Kooij wins Tour de France 5th stage in chaotic sprint finish

Britain's Fery to face Zverev in Wimbledon semi-finals

Britain's Fery to face Zverev in Wimbledon semi-finals

Zverev sees off Fritz to make first Wimbledon semi-final

Zverev sees off Fritz to make first Wimbledon semi-final

Barcelona sets new heat record at 40.7C: weather agencies

Barcelona sets new heat record at 40.7C: weather agencies

'The Pitt,' 'Hacks' lead Emmy nominations

'The Pitt,' 'Hacks' lead Emmy nominations

France lose appeal against Olise booking at World Cup

France lose appeal against Olise booking at World Cup

Putellas joins star cast at London City Lionesses

Putellas joins star cast at London City Lionesses

Oil back at $80, stocks slide as Trump says Iran ceasefire over

Oil back at $80, stocks slide as Trump says Iran ceasefire over

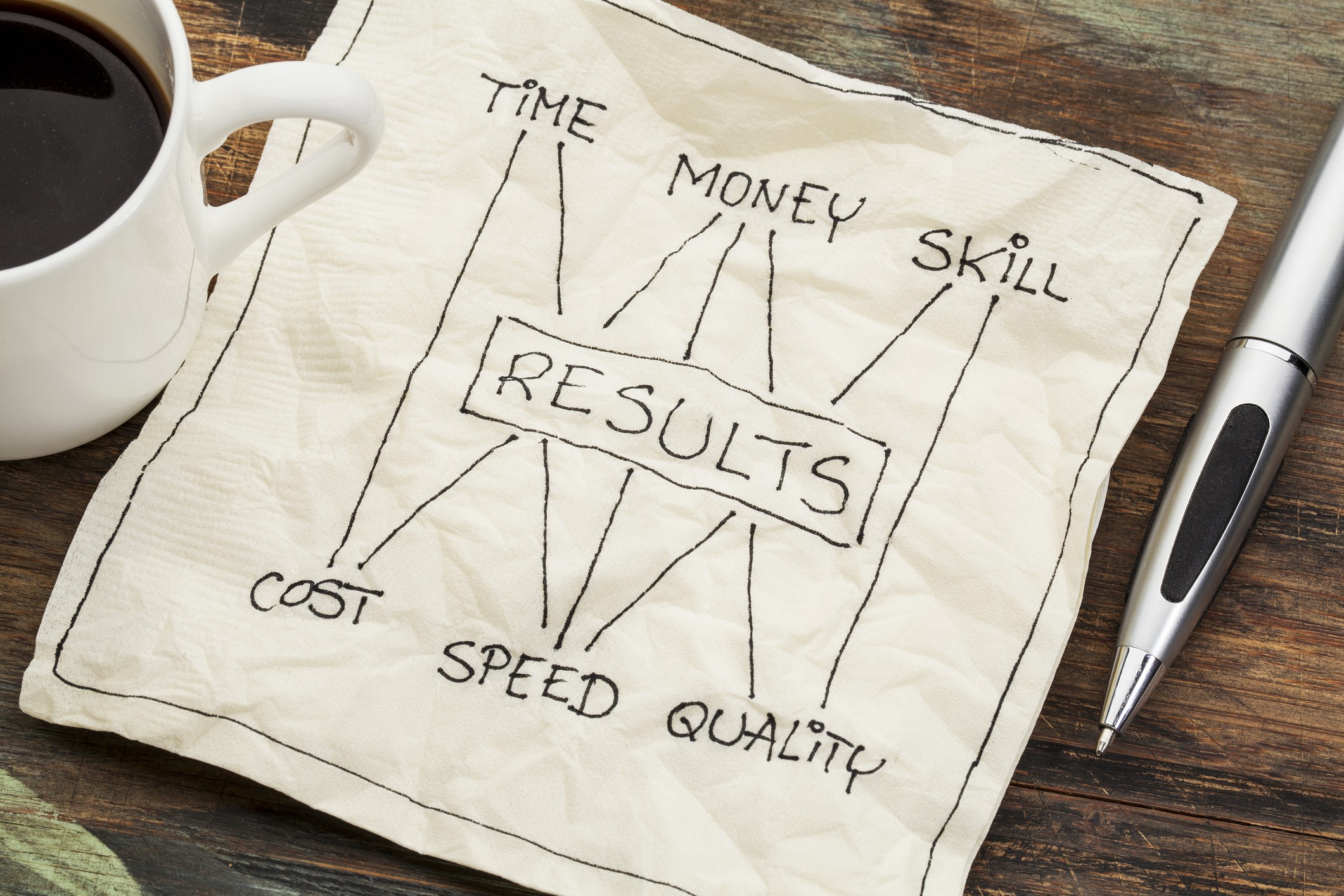

Buying too much life insurance can cause you to pay more on monthly life insurance premiums than you need. However, buying too little can financially strain your loved ones when the death benefit runs out.

While it's impossible to calculate your future needs perfectly, several strategies can help you estimate your needs to ensure your loved ones have enough coverage without you overpaying. This article explores a few methods for calculating your life insurance coverage, each varying in complexity and accuracy.

1. The 10X Rule

The 10X income method is the simplest way to estimate your life insurance needs. It involves multiplying your current income by 10 to determine your total coverage needs.

For example, if you earn $50,000 per year, you'd get a life insurance policy with a $500,000 death benefit.

Some adjust this to be a 15x rule, multiplying their annual income by 15 instead of 10. While this results in a larger death benefit, it may work if you want to provide support for longer or account for periods of higher inflation.

2. DIME Formula

The DIME formula factors your debts, income, mortgage, and education costs into your coverage needs.

Here's how to calculate your life insurance needs with the DIME formula:

Multiply your annual income by the number of years you want to provide support

Add up all debts, including your remaining mortgage balance

Estimate each dependent's education costs

Add the numbers from 1, 2, and 3.

For example, let's say you earn $50,000 annually and want to provide 10 years of support for your loved ones. Multiply $50,000 by 10 years to get $500,000. This is your "base" number.

Additionally, you have $10,000 in debt and $100,000 left on your mortgage balance. You estimate your child's education costs will total $40,000.

The sum of your debts, mortgage, and education costs is $150,000. Adding this to your $500,000 base number brings you to a total coverage need of $650,000.

The DIME formula is more complex and requires some estimation. However, it leads to purchasing extra coverage that can create greater financial security.

3. Income Replacement Plus Cushion

The Income Replacement Plus Cushion strategy assumes your loved ones won't need to spend the full death benefit upon your death to replace your income.

Instead, they invest the proceeds into conservative investments to preserve the death benefit and use the returns to cover their living expenses. Then, when they no longer need it to cover expenses, they can tap into it for larger goals, such as education or buying a new home.

Calculating your needs with this method involves dividing your income by a conservative estimated rate of return to arrive at your death benefit. For example, imagine you earn $50,000 per year and estimate a 4% average rate of return. Dividing $50,000 by 4% arrives at a death benefit of $1,250,000.

This method may work if your spouse works and earns a decent portion of the household income since they may be able to live on an invested death benefit's earnings. It can also work if your loved ones will receive a substantial estate from you, such as significant investment accounts and retirement funds.

4. Obligations-Earnings Method

The Obligations-Earnings calculates the difference between your future obligations (including your income) and assets to find your needs. Your obligations will outweigh your assets, meaning the difference is the estimated death benefit you need.

This method is the most complex since it accounts for several financial matters, but it can also more accurately estimate your coverage needs.

First, multiply your annual salary by the number of years you want to provide support. Add this amount to the following:

Mortgage balance

Other debts

Future goals and needs, such as, but not limited to, education

Next, subtract your liquid assets from the above sum. Liquid assets include:

Bank accounts (savings, checking)

Current life insurance, if any

Retirement accounts, if accessible to heirs immediately after inheriting

The result represents your estimated life insurance coverage needs.

Determine Your Life Insurance Needs

There are many ways to calculate your life insurance needs, each increasing in complexity but also accounting for more factors to boost accuracy.

Ultimately, using a life insurance calculator may be the easiest way to estimate your coverage needs. These online tools collect much of the information the Obligations-Earnings Method uses but it handles the math for you. This can help you get enough coverage to provide for your loved ones without overpaying for unneeded coverage.

Content within this article is provided for general informational purposes and is not provided as tax, legal, health, or financial advice for any person or for any specific situation. Employers, employees, and other individuals should contact their own advisers about their situations. For complete details, including availability and costs of Aflac insurance, please contact your local Aflac agent.

Aflac coverage is underwritten by American Family Life Assurance Company of Columbus. In New York, Aflac coverage is underwritten by American Family Life Assurance Company of New York.

Aflac life plans - B60000 series: In Arkansas, Idaho, Oklahoma & Virginia, Policies: ICC18B60C10, ICC18B60100, ICC18B60200, ICC18B60300, & ICC18B60400. Not available in Delaware. Q60000 series/Whole: In Arkansas & Delaware, Policy Q60100M. In Idaho, Policy Q60100MID. In Oklahoma, Policy Q60100MOK. Not available in Virginia. Q60000 series/Term: In Delaware, Policies Q60200CM. In Arkansas, Idaho, Oklahoma, Policies ICC18Q60200C, ICC18Q60300C, ICC18Q60400C. Not available in Virginia.

Aflac Final Expense insurance coverage is underwritten by Tier One Insurance Company, a subsidiary of Aflac Incorporated and is administered by Aetna Life Insurance Company. Tier One Insurance Company is part of the Aflac family of insurers. In California, Tier One Insurance Company does business as Tier One Life Insurance Company (Tier One NAIC 92908).

In AR, DE, ID, OK and VA: Policies ICC21-AFLLBL21 and ICC21-AFLRPL21; and Riders ICC21-AFLABR22, ICC21-AFLADB22, and ICC21-AFLCDR22. Aflac Final Expense policies are not available in New York.

Coverage may not be available in all states, including but not limited to DE, ID, NJ, NM, NY or VA. Benefits/premium rates may vary based on state and plan levels. Optional riders may be available at an additional cost. Policies and riders may also contain a waiting period. Refer to the exact policy and rider forms for benefit details, definitions, limitations, and exclusions.

Aflac WWHQ | Tier One | 1932 Wynnton Road | Columbus, GA 31999

Aflac New York | 22 Corporate Woods Boulevard, Suite 2 | Albany, NY 12211

Z2400915 EXP 10/25

CONTACT:

Senior PR & Corporate Communications

Contact: Angie Blackmar, 706-392-2097 or [email protected]

SOURCE: Aflac

A.O.Scott--AT