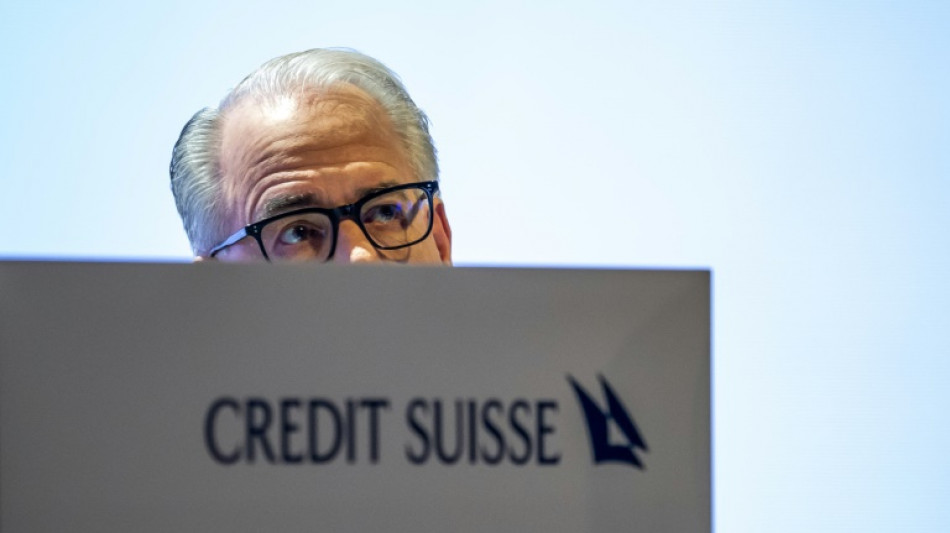

Credit Suisse chiefs say sorry to shocked shareholders / Photo: Fabrice COFFRINI - AFP

'Pragmatists' vs 'hardliners': Is Iran split over US deal?

'Pragmatists' vs 'hardliners': Is Iran split over US deal?

H5 bird flu detected in second Australia state

H5 bird flu detected in second Australia state

Brazil aim for last 32 as World Cup goes into hectic phase

Brazil aim for last 32 as World Cup goes into hectic phase

Necessity drives gold miners in DR Congo's Ebola epicentre

Necessity drives gold miners in DR Congo's Ebola epicentre

Japan PM heckled at WWII memorial

Japan PM heckled at WWII memorial

Hanoi residents mount silent protest over home demolitions

Hanoi residents mount silent protest over home demolitions

US Congress passes symbolic Iran war rebuke to Trump

US Congress passes symbolic Iran war rebuke to Trump

Bolivia's government is 'stoking a civil war,' ex-president Evo Morales tells AFP

Bolivia's government is 'stoking a civil war,' ex-president Evo Morales tells AFP

Fans in China put politics aside to cheer Japan at World Cup

Fans in China put politics aside to cheer Japan at World Cup

Geopolitics and AI in spotlight at China's 'Summer Davos'

Geopolitics and AI in spotlight at China's 'Summer Davos'

Race for robotaxi market arrives in London

Race for robotaxi market arrives in London

Moana Pasifika axed from Super Rugby after rescue talks fail

Moana Pasifika axed from Super Rugby after rescue talks fail

Golden Boot battle steals the show at World Cup

Golden Boot battle steals the show at World Cup

Red or green? For Brazil, the politics of World Cup kits matter

Red or green? For Brazil, the politics of World Cup kits matter

AQP One Introduces BioBaseline(TM) as a Foundational Standard for Physiological Intelligence

AQP One Introduces BioBaseline(TM) as a Foundational Standard for Physiological Intelligence

InterContinental Hotels Group PLC Announces Transaction in Own Shares - June 24

InterContinental Hotels Group PLC Announces Transaction in Own Shares - June 24

Andes Health Mart Pharmacy Honored as IPC's 2026 Most Valuable Pharmacy

Andes Health Mart Pharmacy Honored as IPC's 2026 Most Valuable Pharmacy

US Congress passes landmark housing affordability bill

US Congress passes landmark housing affordability bill

Dream job: US soccer fans paid to watch every World Cup game

Dream job: US soccer fans paid to watch every World Cup game

Europe wilts under record heat as AC sales soar

Europe wilts under record heat as AC sales soar

Rubio rejects Iran tolls on Hormuz as deal strains multiply

Rubio rejects Iran tolls on Hormuz as deal strains multiply

Cubans bid farewell to revolution hero Valdes

Cubans bid farewell to revolution hero Valdes

Ronaldo delights in silencing 'attacks' after making World Cup history

Ronaldo delights in silencing 'attacks' after making World Cup history

'Paris in this heat is awful': Tourists change plans as sites close early

'Paris in this heat is awful': Tourists change plans as sites close early

'I'm back': Ronaldo scores at sixth World Cup as Portugal run riot

'I'm back': Ronaldo scores at sixth World Cup as Portugal run riot

Credit Suisse chairman Axel Lehmann said Tuesday he was "truly sorry" that the beleaguered bank could not be saved as he faced angry and tearful shareholders whose money has gone up in smoke.

Credit Suisse's chiefs fronted up at the bank's annual general meeting, 16 days after its hastily-arranged takeover by larger Swiss rival UBS -- a mega-merger in which the shareholders of both banks had no say at all.

The 167-year-old bank's final AGM was the first chance Credit Suisse shareholders had to voice their frustrations, and some turned up in tears as they counted the cost of the bank's implosion.

"I can understand the bitterness, the anger and the shock of all those who are disappointed, overwhelmed and affected by the developments," Lehmann said at the Hallenstadion, Zurich's biggest indoor arena.

With the bank's share price in free-fall and fearing an imminent collapse that could have triggered an international banking crisis, the Swiss government, the central bank and the financial regulators strongarmed UBS into taking over Credit Suisse on March 19.

"We wanted to put all our energy and our efforts into turning the situation around," said Lehmann, who was brought in as chairman in January 2022 to fix the bank following a string of scandals that sapped investor confidence.

"It pains me that we didn't have the time to do so and in that fateful week in March our plans were thwarted -- and for that I am truly sorry," he said.

"I apologise that we were no longer able to stem the loss of trust that has accumulated over the years and for disappointing you."

- Family's money evaporated -

Thanks to those scandals, shareholders have seen the value of their investment plunge from 12.78 Swiss francs per share in February 2021 to the 0.76 francs they will receive in the $3.25-billion merger.

"I am angry and I lost 10,000 Swiss francs ($11,000). It's not so much but it's not good. It's (a lot of) money for my family," Stephan Denzler told AFP, tears forming in his eyes.

"This is a historical moment and this the reason that I want to be at this assembly."

Chief executive Ulrich Koerner said it would be the bank's last ordinary general meeting.

UBS -- which faces its own annual general meeting in Basel on Wednesday -- is the biggest bank in Switzerland, with Credit Suisse in second place.

They are both among the 30 worldwide Global Systemically Important Banks -- deemed of such importance to the international banking system that they are considered too big to fail.

But the markets saw Credit Suisse -- which suffered a net loss of $7.9 billion in 2022 -- as a weak link in the global chain following the collapse of three US regional banks in early March.

- 'Deep personal regret': CEO -

The bank's share price plunged by more than 30 percent on March 15 to a record low of 1.55 Swiss francs.

Despite reassurances, shares recovered little ground to close the week at 1.86 francs on March 17.

Fearing what might happen when the markets reopened on March 20, the Swiss government then sprung into action to patch a deal together with UBS.

Credit Suisse has been a part of Switzerland's national identity for 167 years, but nevertheless, "the bank could not be saved", Lehmann insisted.

"Ultimately there were only two options: deal or bankruptcy. The merger had to go through. The terms had to be accepted."

Koerner said he was deeply saddened at the end of Credit Suisse, but said the takeover by UBS was the only feasible solution.

"This fills me with sorrow," he said.

"This is a matter of deep personal regret to me. But the bank's survival was at stake and we... no longer had a choice.

"The collapse of Credit Suisse would have been disastrous, not just for Switzerland but for the global economy at large."

T.Perez--AT